Advertisement

Advertisement

U.S. Wholesale Inflation Cools Again—Is a Fed Pivot Now on the Table?

By:

Key Points:

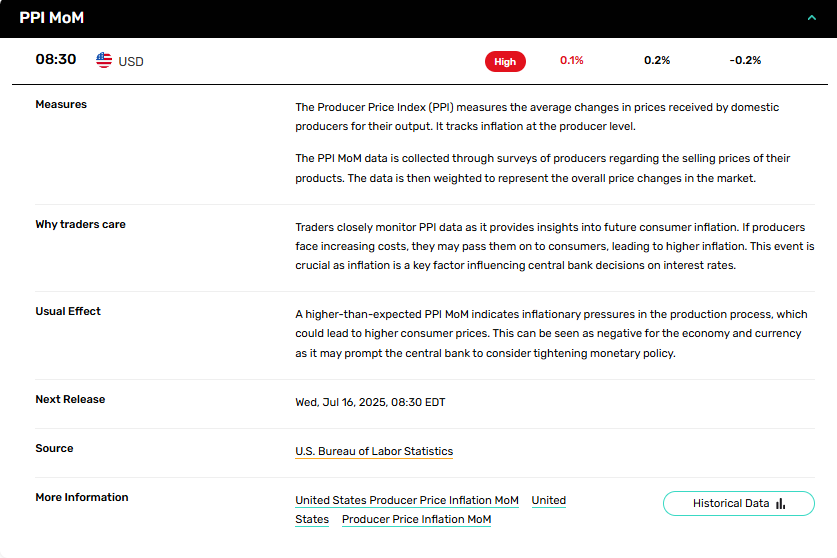

- U.S. PPI rose just 0.1% in May, missing the 0.2% forecast, signaling softer wholesale inflation pressures.

- Core PPI—excluding food and energy—also rose only 0.1%, undercutting the expected 0.3% rise, easing Fed pressure.

- With wholesale inflation below target, traders expect a dovish Fed stance, pressuring USD and lifting equities.

PPI Misses Forecasts: Federal Reserve Policy Implications Grow

U.S. wholesale inflation rose less than expected in May, signaling modest cost pressures that could influence upcoming Federal Reserve decisions. The Producer Price Index (PPI) for final demand advanced just 0.1%, falling short of economists’ expectations for a 0.2% rise, while the core PPI—excluding food and energy—also rose 0.1%, undercutting the 0.3% estimate.

Final Demand Goods Hold Steady, Energy Flat

Goods inflation remained contained in May. The PPI for final demand goods increased 0.2%, driven primarily by a 0.2% rise in core goods, while food prices ticked up 0.1% and energy prices were unchanged. Volatile components such as jet fuel, down 8.2%, and pork prices, also lower, offset gains in tobacco (+0.9%) and roasted coffee. Weakness in energy markets, combined with flat pricing in essential categories, suggests limited upstream pressure on consumer prices.

Services Margins Up, But Broader Prices Flat

On the services side, the PPI rose 0.1%, supported by a 0.4% increase in trade margins—especially machinery and vehicle wholesaling, which surged 2.9%. However, core services excluding trade, transportation, and warehousing saw no monthly change. Declines in airline fares (-1.1%) and weakness in financial services fees kept broader service inflation contained, supporting the case for restrained demand-side inflation.

Core PPI Trends Signal Easing Pressures

The annual rise in the core PPI (excluding food, energy, and trade services) stands at 2.7%, in line with the Fed’s comfort zone. May marks a deceleration from April’s 0.1% monthly decline, but the bounce remains soft. Importantly, unprocessed goods for intermediate demand fell 1.6%, indicating that upstream input costs are not rebounding, with natural gas prices plummeting 18.7%.

Fed Outlook: Dovish Tilt Likely to Strengthen

With both headline and core inflation underperforming forecasts, pressure on the Fed to maintain a hawkish stance has eased. The data support a more patient monetary policy approach, especially as forward-looking indicators, including intermediate goods prices, trend lower. Unless upcoming CPI figures surprise to the upside, this release strengthens the case for holding rates steady.

Market Forecast: Bearish USD, Bullish Equities

Given the soft inflation readings, expect a bearish bias for the U.S. dollar, particularly against peers with tighter inflation profiles. Equities may get a modest boost from lower rate expectations, especially in rate-sensitive sectors like technology and real estate. Treasury yields are also likely to drift lower, supporting bond prices in the short term.

About the Author

James HyerczykProfits & Punchlines

Mr.Hyerczyk is a technical analyst, market researcher, educator and trader. Jim is an expert in the area of patterns, price and time analysis, Forex and stocks.

Advertisement